Commentary

This week, one of the world’s foci must be the potential U.S. government default on its debt. In most circles, this continues to progress as if we have never encountered such a situation before. But this might not be true. According to Terry Zivney and Richard Marcus of The Financial Review, “Investors in T-bills maturing April 26, 1979, were told that the U.S. Treasury could not pay on maturing securities to individual investors. The Treasury was also late in redeeming T-bills, which became due on May 3 and May 10, 1979.”

“The Treasury blamed this delay on an unprecedented volume of participation by small investors, on the failure of Congress to act in a timely fashion on the debt ceiling legislation in April 1979, and on an unanticipated failure of word processing equipment used to prepare check schedules.” One can see such “technical default,” or in effect “technical delay,” is quite similar to what is being encountered now. In either case, the default, if any, is neither intentional nor fundamental. What would be the outcome? The first to check is the Treasury yield (T-yield).

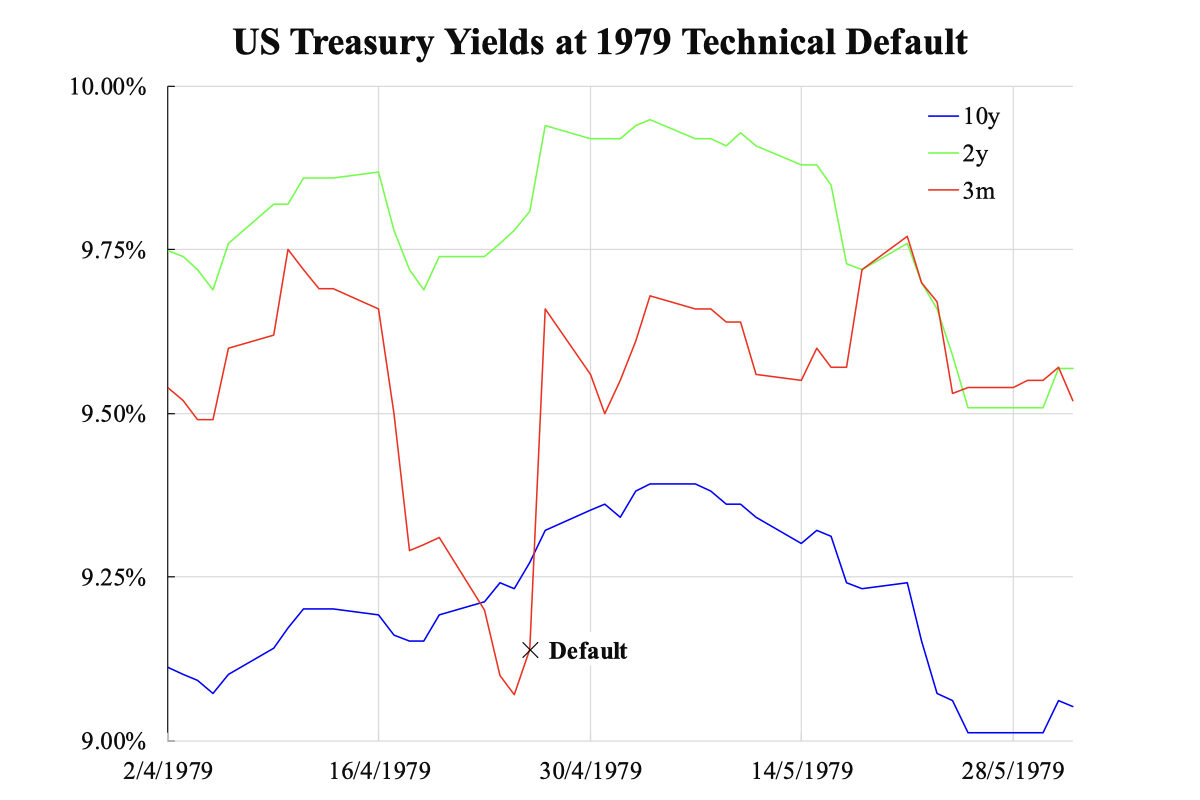

The accompanying chart shows three tenors of T-yield around 1979 technical default. Since it was bills (up to one year) being defaulted, the impacted tenor should be three-month. The two most active tenors—two-year and ten-year bills—are also compared. Only the three-month T-yield shot up by about 50 basis points, while the other two tenors remained a steady increase against the backdrop of over ten percent CPI year-on-year inflation. Note the similarity of the yield curve inversion, where the recession was followed in about three quarters.

This was in sharp contrast to Greece’s default in Spring 2012, where the two-year sovereign yield shot up to double digits by 2010 and to triple digits by the Fall of 2011. In this case, Greece was insolvent while the U.S. was illiquid; the market would treat these differently. So long as the Treasury yield curve remains overall contained, a domino effect could be avoided. In the past two quarters, the portion of the two-year and longer-end yield curves have been declining. Even the three-month tenor has been tightly following the policy rate at around 5.25 percent level.

This is certainly not any symptom of a debt crisis. The bond market is full of intelligent guys and smart money. A sharp spike to yield until default happens will be highly unlikely. Early selling always makes sense theoretically, particularly when news about a default has been on the table for some time.

Since the projected probability of technical default is not negligible, the unexceptional calm of the yield curve might confirm the 1979 experience where even if a default happened, there might not be any big reaction. Such a scenario seems likely.

In this big debt era, default is no longer equivalent to doomsday. Greece did default with a three-quarter debt haircut, yet Euro is still there after a decade of that happening. Bond traders might be proved correct.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

{kind=link}