From the latest dot plot released by the Federal Reserve, the mode value of funds rate implies two more hikes of a quarter percent by yearend. However, careful examination shows there are more dots below the mode than above. Taking into account the dovish tone by chairman Powell, the market does not believe this and still expects only one more ¼ percent hike to complete the cycle. Nevertheless, recent experience shows the “expiry date” of the Fed’s dot plot is very short, so they can change their mind as soon as a few days after the Federal Open Market Committee meeting.

The emphasis on deciding the policy rate “meeting by meeting” means they have no grasp at all on the near-term future outlook. On one hand, they are scared by the curse of an inverted yield curve (especially the one this time, which is exceptionally deep) as well as the banking crisis in March, but on the other hand, they are worried about the strong consumption and jobs markets as well as the highly persistent wage and price inflations. Given they have a track record of revising the dots upward many times before, raising these further is certainly something on the table.

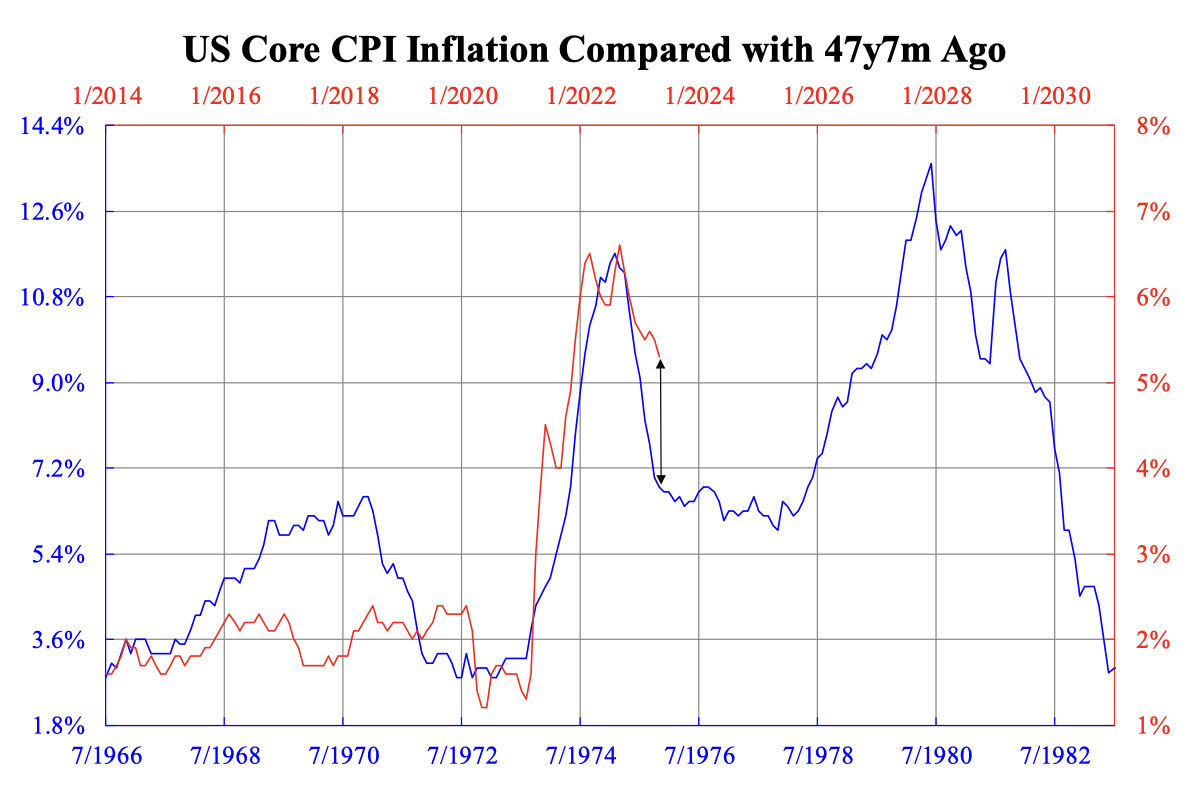

The inflation downtrend is indeed less optimistic than it seems. Although the recent overall consumer price index (CPI) year-over-year (YoY) inflation did fall like the downtrend in 1975 (recall our chart published on April 13), the core one did not. The accompanying chart presents this. One can see the latest core inflation persistence is, in fact, worse than that in the mid-1970s. Had history been repeating, the core inflation by now should have come down to below four percent; yet, in fact, it is still above five percent. What makes the deviation different from the historical path?

Look back at what Fed did in the mid-1970s. Although the Fed chairman Arthur Burns suffered severe criticism for not doing the right thing under political pressure, the policy rate was consistently higher than overall inflation by 2-3 percent most of the time when inflation surged. By sharp contrast, Jay Powell let the policy rate run behind inflation by over eight percent. Only in the last month did the policy rate first surpass inflation, turning the real interest rate positive. With such an insincere approach to tightening, inflation would unsurprisingly remain sticky.

Based on the experience of the mid-1970s, when inflation became high, say over five percent, an even higher policy rate by 2-3 percent still took exactly 1.5 years to bring inflation down. Alternatively, chairman Paul Volcker shot the policy rate to above inflation by five percent in order to stop the spiral. In either case, the cost of high inflation increased disproportionately and it lasted for too long.

Now, even with 50 basis points more to go and assuming core inflation to fall a bit more, the policy rate will not be well above inflation by then. Unless a recession arrives or some sort of crisis breaks out, the hike cycle cannot just stop there and must be continued or inflation will just stay high at the current level.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

{kind=link}