Commentary

Debate continues as to whether recession still lies ahead. The yield curve has pointed to an 80 percent chance of recession. But, when comparing today’s situation with the comparable U.S. real GDP contraction in 2008, its timing forecast has low accuracy.

As the original literature documented, the yield curve only predicts a yes-no outcome (of recession) rather than the deepness and timing of it, if any. Moreover, the more accurate a prediction of an outcome usually leads to a less accurate prediction of its timing. And intuitively, a longer-range indicator will provide less detail about its predicted nature.

To see a broader picture with greater accuracy, other indicators can fill in the gaps. Housing indicators are an effective tool used in recession prediction. However, it may not be relevant now. Although investment is usually the key driver of economic (GDP) growth where housing is a major investment sector, the length of the housing cycle is usually a multiple of business cycles. Sometimes there are economic recessions without a housing recession (1990 was one example). Housing indicator predictions may therefore fail to produce a signal for all recessions.

Looking at broader investment types, overall investment growth will likely coincide with the economic cycle, rendering it useless for predicting a recession. Much effort has been made to discover the early warning signals of a recession, but most methods rely on market information. Even the leading indicator compiled by the Conference Board utilizes stock market data. Despite the yield curve being produced this way, the heavy reliance on the market (especially the stock market) could lead to a fast-changing outcome, making it a much less reliable indicator.

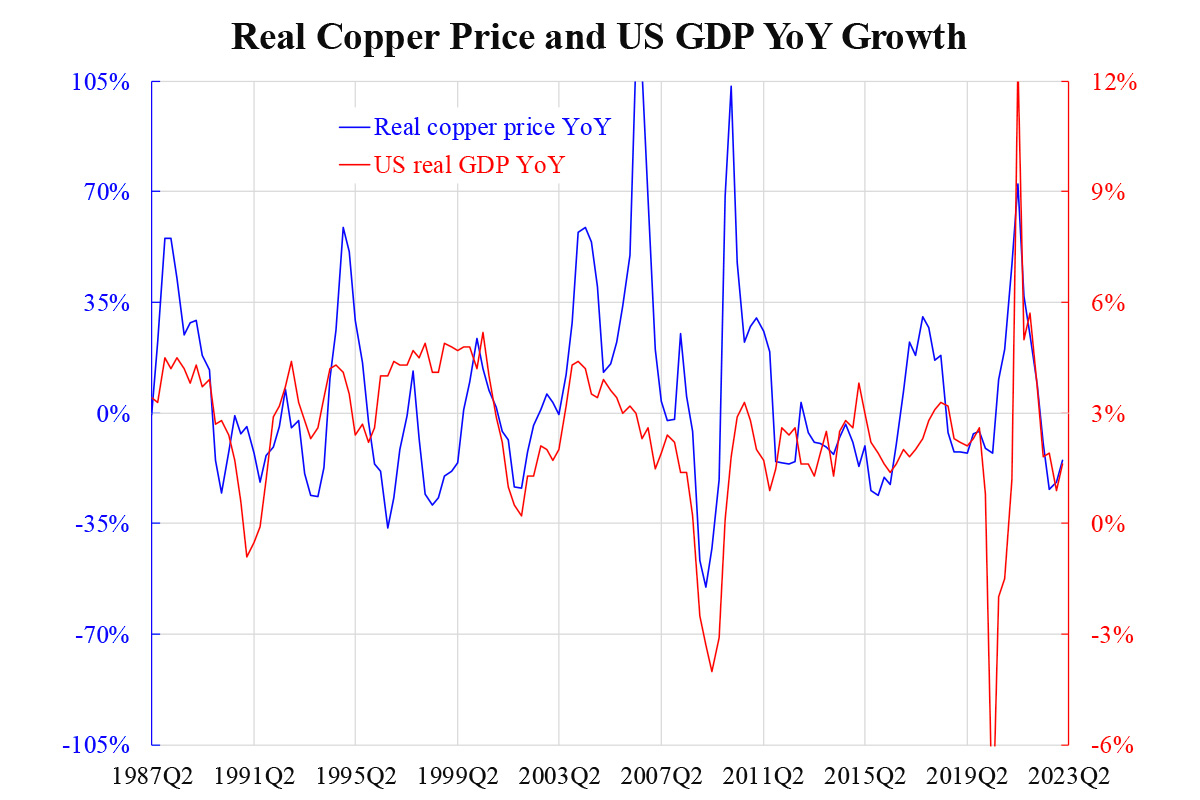

One commonly used indicator is the price of copper, often labelled as “Dr” in projection. The accompanying chart shows its movements with U.S. real GDP year-on-year growth. If the price factor of copper is used as a meaningful predictor, the real price should be used rather than the nominal price.

Also, the real price growth should be used to predict the real GDP growth. Deflating a nominal copper price could simply use U.S. CPI. We are dealing with U.S. data, but predictions for other countries can also be made given the similar economic cycles. One can therefore see that copper has no predictive power to determine the onset of a recession.

The reason for this is simple. Copper and other raw materials (like crude oil) are affected by factors of production. These commodities are only required when a final demand calling for production exists.

Although entrepreneurs generally invest and produce ahead of demand, observation suggests that the time gap between supply and demand is not too long. Accordingly, the correlation between the real copper price and real GDP growth rates is getting higher, the two are almost coincidental, meaning that there is not much information to be extracted.

Compared to the longer-range yield curve predictor, it seems that most short-term indicators cannot be relied upon. It is, therefore, unwise to insist on knowing the exact timing of a collapse, given indicators’ very chaotic and highly unpredictable nature.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

{kind=link}